Twenty years in power. Three curves. One convergence.

In the middle of 2005 I walked into my first power station. The Linden cogeneration plant in New Jersey: 940MW of gas burning around the clock, selling most of its output into New York City. Goldman Sachs owned it at the time, and I was just starting on the commodities trading floor. Combined heat and power was the clever asset to own, the cool kid on the block. If you wanted to be sophisticated about energy in 2005, you owned a combined cycle gas plant.

Linden CHP plant

That year, global installed solar capacity was a rounding error. Wind was a curiosity. Grid scale batteries did not meaningfully exist.

Two other things happened in 2005 that had nothing to do with each other, and nothing to do with Linden or the energy world.

A small company called Tesla raised its Series B and signed a deal with Lotus to build an electric sports car out of ~7000 laptop battery cells. Most serious people thought it was absurd.

First Tesla battery pack

In that same year, a neuroscientist named Demis Hassabis shut down his video games startup Elixis Studios and went back to do a PhD on brain neuroscience. AI was still a vague idea championed by then unknown professors in North America, even if GPUs were already powering PlayStations. No one in energy had heard of these people.

Three corners of the economy. A gas plant, a car battery, video games. No connection between any of them.

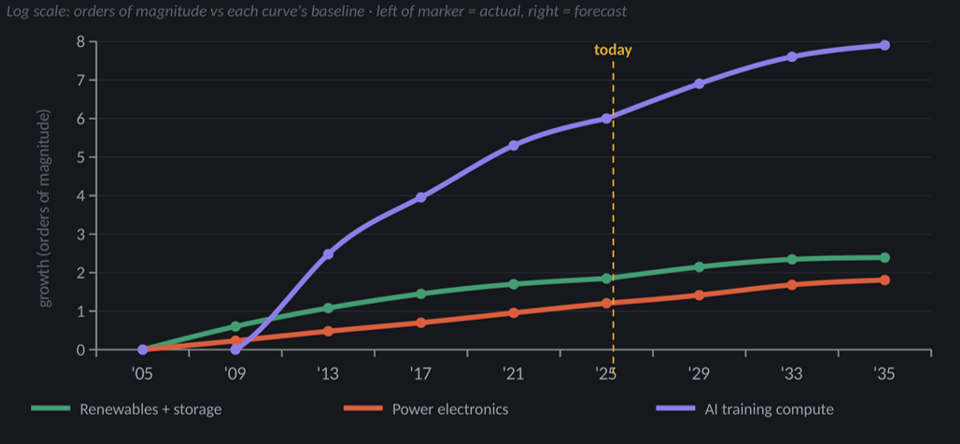

I want to show you what each of those corners did over the next twenty years, because all three of the technologies they seeded turned out to be exponential. And exponentials are the only thing that matters.

Curve one. Solar, wind and storage.

When I started, solar modules were around $4 a watt. Today they are under 30 cents. This is the same kind of learning curve that governs chips. Every time the world doubles cumulative production, the price drops by about a fifth. It has held for forty years and across a fall of more than 99%.

Batteries did the same thing. Lithium-ion packs were over $1,000 per kWh when Tesla was stuffing them into a Lotus. They are around $100 now. The gas plant I admired in 2005 is the expensive option today.

This curve is now so well understood that it is almost boring to talk about. That is exactly the point. What was a heroic bet in 2005 is now arithmetic. The interesting money has already moved on from asking whether cheap clean electrons win. They do. The question is what you build on top of them.

Curve two. Power electronics.

This is the one nobody talks about, and it is my favourite. In the background there is an industrial Moore's Law for power electronics. Power density roughly doubles every four years. The kit that moves and converts electricity, the inverters and converters, has been getting smaller, cheaper and more efficient on a relentless curve for decades.

What turbocharged it was wide bandgap (WBG) semiconductors. Silicon carbide and gallium nitride took over the chargers and converters. These materials switch faster, run hotter and waste far less energy than the silicon they replaced. The result is that the box which used to be the size of a fridge is now the size of a briefcase, and the briefcase costs less and loses less of your power as heat.

If you want to know why this matters, think about what it lets you put in places you never could before. A converter efficient and small enough to live inside a wall charger, a rooftop unit, a car. The intelligence in an energy system has to live next to the power electronics. Shrink the electronics and you change where the intelligence can go.

Curve three. Artificial intelligence.

Hassabis finished his PhD, and the games chip and the brain collided. In 2012, ImageNet showed that neural networks trained on Nvidia gaming GPUs could suddenly see. In 2016, DeepMind beat the world champion at Go, something people had said was a decade away. The video game chip became the most important industrial input on Earth.

We all know where this curve went next. What matters for energy is less the frontier models and more the cheap inference now possible at the edge. The same trajectory that made the GPU indispensable in the data centre is making capable intelligence affordable in a wall mounted box drawing a few watts.

The convergence

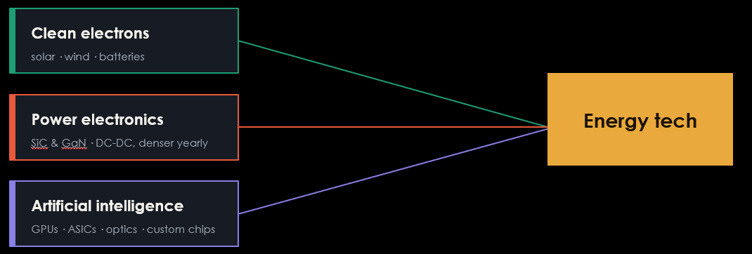

Three corners that did not know each other in 2005. Here is the whole point of having lived through it.

Energy tech today is the convergence of all three. A modern electrified asset is cheap clean electrons, controlled by exponentially better power electronics, optimised by AI. The car in 2005 needed all three and none existed at scale. Today the battery is cheap, the silicon carbide inverter is tiny, and the software drives itself.

The convergence already happened in the car. That is the part most people miss. The electric vehicle is not a transport story, it is the first product where all three curves crossed at once and produced something better and cheaper than what it replaced. It is now happening to everything that plugs in.

So what does it mean for venture capital? Three predictions.

One. AI infrastructure decentralises, and the power problem moves to the chip.

The reflex today is to build ever larger gigawatt data centres. With edge inference booming, we will need fewer mega campuses than the current consensus assumes. Entropy will eventually win and most inference will move on prem. But wherever the compute sits, the binding constraint is no longer the model, it is delivering clean power to the silicon without wasting a third of it as heat.

This is why we backed Claros.

They deliver power directly to the processing unit with an integrated voltage regulator and a DC native distribution layer, cutting the conversion losses that the standard architecture treats as a cost of doing business.

The same power electronics curve that shrank the car charger is now being aimed at the most power-hungry machine humans have ever built. Better power delivery at the chip is what unlocks the next generation of data centre performance, and very few people are working on it.

Two. Renewables keep displacing fossil fuels.

This one is boring and almost done. Cheap wins.

Three, and this is where I would put my attention. The grid is the last thing the convergence has not touched.

The power electronics revolution is behind the hottest set of semi assets in public markets today, and we love it, but it has barely reached the distribution grid. The low voltage grid is still largely the dumb, analogue machine it was when I walked into Linden. The same convergence that remade the car is going to reshape how homes consume, store and trade power.

This is the Ohme thesis. Dave Watson and I first met in 2017, both staring at the first boom of front of meter batteries and imagining a grid where the cars themselves became the storage backbone, without the expensive capex. He had the conviction to build the software layer for the distribution grid, and the discipline to start with hardware so that Ohme controlled the asset rather than being at the mercy of whoever else owned it. Today, Ohme runs the world’s second largest aggregated fleet of distributed assets. That is no longer a charging business. It is grid infrastructure that operators will have to plan around, built quietly out of cars while everyone else was looking at substations.

That is the trade. The car already proved the thesis end to end. Claros is the convergence aimed at the chip, Ohme is the convergence aimed at the grid edge, and the distribution grid is the next twenty years. Few are priced for it.

I started in a gas plant that everyone agreed was the future. It was the past, and I could not see it yet. The lesson of twenty years is that the important curves are the ones running quietly in corners you are not paid to watch. Three of them just met. Watch what they touch next.